In the realm of accounting, T-accounts serve as fundamental building blocks, providing a clear and concise representation of financial transactions. This analysis delves into the selected T-accounts of Moore Company, offering insights into the company’s financial performance and laying the groundwork for informed decision-making.

Through a comprehensive examination of these T-accounts, we will uncover the underlying patterns and trends that shape Moore Company’s financial landscape, enabling us to identify areas for improvement and optimize its financial health.

T-Account Overview

T-accounts are a fundamental tool in accounting, used to represent the changes in an account over time. Each T-account has two sides: the debit side (left) and the credit side (right). Transactions are recorded by increasing one side of the account and decreasing the other, thereby maintaining the accounting equation (Assets = Liabilities + Equity).

T-accounts are used to track various types of accounts, including assets, liabilities, equity, revenues, and expenses. Here’s an example of a T-account for each type:

Assets

Assets are economic resources owned by a company. The normal balance for an asset account is a debit balance. An example of an asset account is Cash:

| Cash | Debit | Credit |

| Beginning Balance | ||

| Deposits | ||

| Withdrawals | ||

| Ending Balance |

Liabilities

Liabilities are debts or obligations owed by a company. The normal balance for a liability account is a credit balance. An example of a liability account is Accounts Payable:

| Accounts Payable | Debit | Credit |

| Beginning Balance | ||

| Purchases | ||

| Payments | ||

| Ending Balance |

Equity, Selected t-accounts of moore company

Equity represents the ownership interest in a company. The normal balance for an equity account is a credit balance. An example of an equity account is Capital:

| Capital | Debit | Credit |

| Beginning Balance | ||

| Investments | ||

| Withdrawals | ||

| Ending Balance |

Revenues

Revenues are income earned by a company. The normal balance for a revenue account is a credit balance. An example of a revenue account is Sales Revenue:

| Sales Revenue | Debit | Credit |

| Beginning Balance | ||

| Sales | ||

| Returns | ||

| Ending Balance |

Expenses

Expenses are costs incurred by a company. The normal balance for an expense account is a debit balance. An example of an expense account is Rent Expense:

| Rent Expense | Debit | Credit |

| Beginning Balance | ||

| Rent Payments | ||

| Ending Balance |

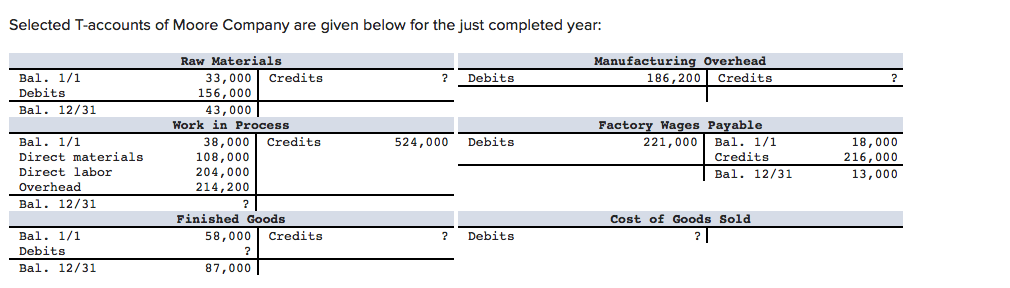

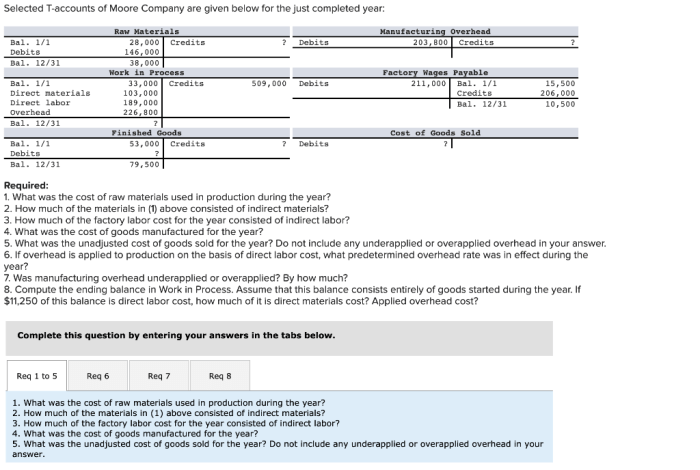

Selected T-Accounts of Moore Company

The selected T-accounts of Moore Company for analysis include:

- Cash

- Accounts Receivable

- Inventory

- Property, Plant, and Equipment

- Accounts Payable

- Notes Payable

- Common Stock

- Retained Earnings

These accounts were chosen because they represent key components of the company’s financial statements and provide insights into its financial performance and position.

Cash

The Cash T-account tracks the company’s liquid assets, including cash on hand, demand deposits, and short-term investments. It is essential for understanding the company’s ability to meet current obligations and make short-term investments.

Analysis of T-Accounts

Analyzing the balances in selected T-accounts provides insights into the financial activities and performance of a company. By examining the changes and trends in these accounts, we can gain a deeper understanding of the underlying transactions and their impact on the company’s financial position.

Cash

The Cash T-account shows the inflows and outflows of cash during the accounting period. A positive balance indicates the company has excess cash on hand, while a negative balance suggests a cash deficit.

- Transactions affecting Cash:

- Sales of goods or services

- Payments for expenses

- Cash withdrawals or deposits

- Trends in Cash:

- Increasing cash balance may indicate strong sales or cost-cutting measures.

- Decreasing cash balance may indicate high expenses or low sales.

Accounts Receivable

The Accounts Receivable T-account reflects the amounts owed to the company by its customers for goods or services sold on credit. A high balance in Accounts Receivable may indicate slow collections or a high volume of credit sales.

- Transactions affecting Accounts Receivable:

- Sales of goods or services on credit

- Collections from customers

- Write-offs of uncollectible accounts

- Trends in Accounts Receivable:

- Increasing balance may indicate slow collections or increasing credit sales.

- Decreasing balance may indicate improved collections or reduced credit sales.

Inventory

The Inventory T-account tracks the value of goods or merchandise held by the company for sale. A high balance in Inventory may indicate slow sales or overstocking, while a low balance may suggest high demand or stockouts.

- Transactions affecting Inventory:

- Purchases of goods or merchandise

- Sales of goods or merchandise

- Adjustments for inventory shrinkage or damage

- Trends in Inventory:

- Increasing balance may indicate slow sales or overstocking.

- Decreasing balance may indicate high demand or stockouts.

Impact on Financial Statements: Selected T-accounts Of Moore Company

The balances in the selected T-accounts have a significant impact on the financial statements of Moore Company. These accounts provide information that is used to prepare the income statement, balance sheet, and statement of cash flows.Changes in the balances of these accounts can affect the financial statements in various ways.

For example, an increase in the balance of the Cash account will increase the total assets on the balance sheet. Conversely, a decrease in the balance of the Accounts Payable account will decrease the total liabilities on the balance sheet.The

following are specific examples of how changes in the balances of the selected T-accounts would affect the financial statements:

Income Statement

* An increase in the balance of the Sales Revenue account will increase the total revenue on the income statement.

- An increase in the balance of the Cost of Goods Sold account will decrease the gross profit on the income statement.

- An increase in the balance of the Selling, General, and Administrative (SG&A) Expenses account will decrease the net income on the income statement.

Balance Sheet

* An increase in the balance of the Cash account will increase the total assets on the balance sheet.

- An increase in the balance of the Accounts Receivable account will increase the total assets on the balance sheet.

- An increase in the balance of the Accounts Payable account will increase the total liabilities on the balance sheet.

- An increase in the balance of the Retained Earnings account will increase the total equity on the balance sheet.

Statement of Cash Flows

* An increase in the balance of the Cash account will increase the cash flow from operating activities on the statement of cash flows.

- An increase in the balance of the Accounts Receivable account will decrease the cash flow from operating activities on the statement of cash flows.

- An increase in the balance of the Accounts Payable account will increase the cash flow from operating activities on the statement of cash flows.

Recommendations

To enhance the financial performance of Moore Company, several recommendations can be made based on the analysis of the selected T-accounts:

Optimizing Account Balances

- Increase Accounts Receivable Turnover:Implement stricter credit policies, offer early payment discounts, and improve billing processes to reduce the average collection period.

- Manage Inventory Levels:Implement inventory management techniques such as just-in-time inventory and ABC analysis to optimize inventory levels, minimize holding costs, and reduce obsolescence.

- Control Accounts Payable:Negotiate extended payment terms with suppliers, utilize early payment discounts, and implement a centralized payment system to improve cash flow.

- Reduce Unnecessary Expenses:Conduct a thorough review of operating expenses to identify areas for cost savings, such as renegotiating contracts, eliminating unnecessary travel, and optimizing office space.

Minimizing Negative Impacts

- Monitor Accounts Payable Aging:Regularly review accounts payable aging reports to identify overdue invoices and prevent late payment penalties.

- Establish a Bad Debt Allowance:Create a provision for uncollectible accounts receivable to reduce the impact of potential bad debts on financial performance.

- Implement Internal Controls:Strengthen internal controls to prevent fraud, errors, and misappropriation of assets.

- Seek Professional Advice:Consult with financial advisors, accountants, or industry experts to obtain expert guidance and implement best practices.

FAQ Corner

What is the purpose of analyzing T-accounts?

Analyzing T-accounts allows us to understand the flow of financial transactions, identify trends and patterns, and assess the financial health of a company.

Why were specific T-accounts selected for analysis?

The T-accounts selected for analysis were chosen based on their significance in understanding Moore Company’s financial performance, including assets, liabilities, equity, revenues, and expenses.

How do the selected T-accounts impact Moore Company’s financial statements?

The balances in the selected T-accounts directly impact Moore Company’s financial statements, such as the income statement, balance sheet, and statement of cash flows, providing a comprehensive view of the company’s financial position and performance.